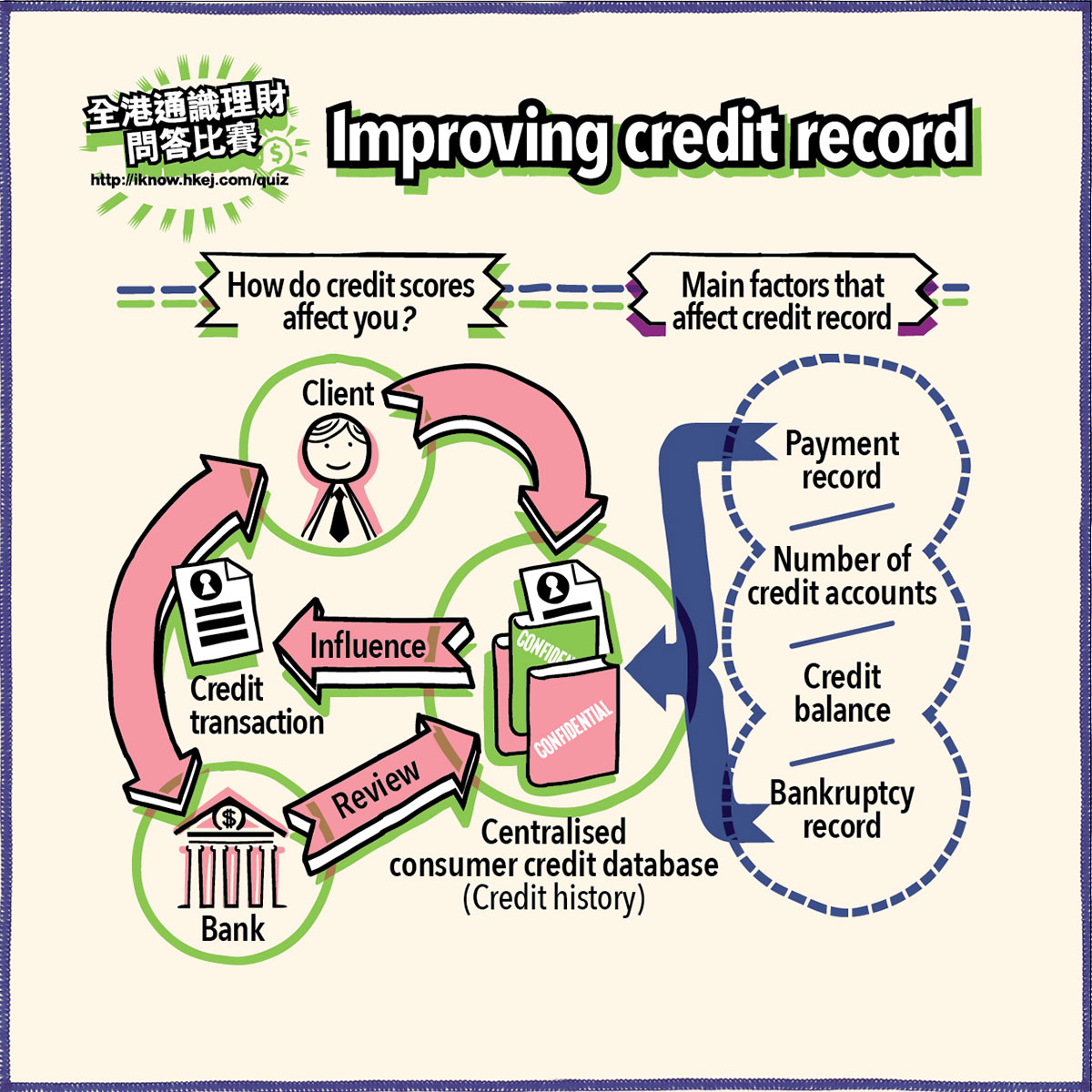

Consumers will have a credit record showing their credit and repayment information, including default repayment record and bankruptcy record, in a centralised consumer credit database once they have used credit products such as credit cards and loans (e.g. car loans, tax loans). For financial institutions like banks, credit card institutions and financial companies, a credit record reflects an individual’s credibility, and is used to determine the depth or diversity of services to be provided, or whether the services will be provided. For example, people who often make repayments late or have long-term low account balances are more difficult to apply for a large loan from banks. Therefore, credit record affects the quality of financial services enjoyed by individuals and even future career development.

Personal credit record is directly associated with the financial services you can obtain, such as personal loan, account opening, and the interest rate that you may be charged; it is closely related to personal financial management, academic and career development, as well as the accomplishment of your life goals. A poor credit record may also affect your career development, as applicants’ credit records are also reviewed by some employers when assessing the applicants’ suitability for certain types of positions (e.g. accounting, credit analysis and approval-related work, etc.). Thereby, you should note the importance of having a good credit record in the long-run. The following are the main factors that affect credit record:

Always make timely and full repayments for personal credit products. Frequent late payments and default records will reduce your credit score.

Fewer credit cards or personal loans may imply financial stability and reliability which helps improve credit score.

Personal loan balance and the number of default payments can affect your credit score.

Those who have filed for bankruptcy usually have poor credit records.

A good credit record may lead to a better interest rate and terms. In contrast, a consumer may be subject to a higher interest rate or get a smaller loan approved, or even his/her loan application may be rejected if his/her credit record is not good. Therefore, it is necessary to have a proper financial plan and avoid overspending to maintain a good credit record.

The recent application for a bank credit card by Little Thrifty’s dad was rejected due to his bad credit score. It turned out that Little Thrifty’s dad has been just making “minimum payment” when settling the bills of his other credit cards, which affects his credit record. If a repayment defaults for more than 60 days, the consumer credit database will retain the default record for five full years from the date of full settlement. Little Thrifty then encourages his dad to settle his credit card bills in full to improve the credit score.

Financial Knowledge

Life Events

Contact Us

In support of the Hong Kong Money Month

Copyright © 2023 Hong Kong Economic Journal Company Limited. All rights reserved.