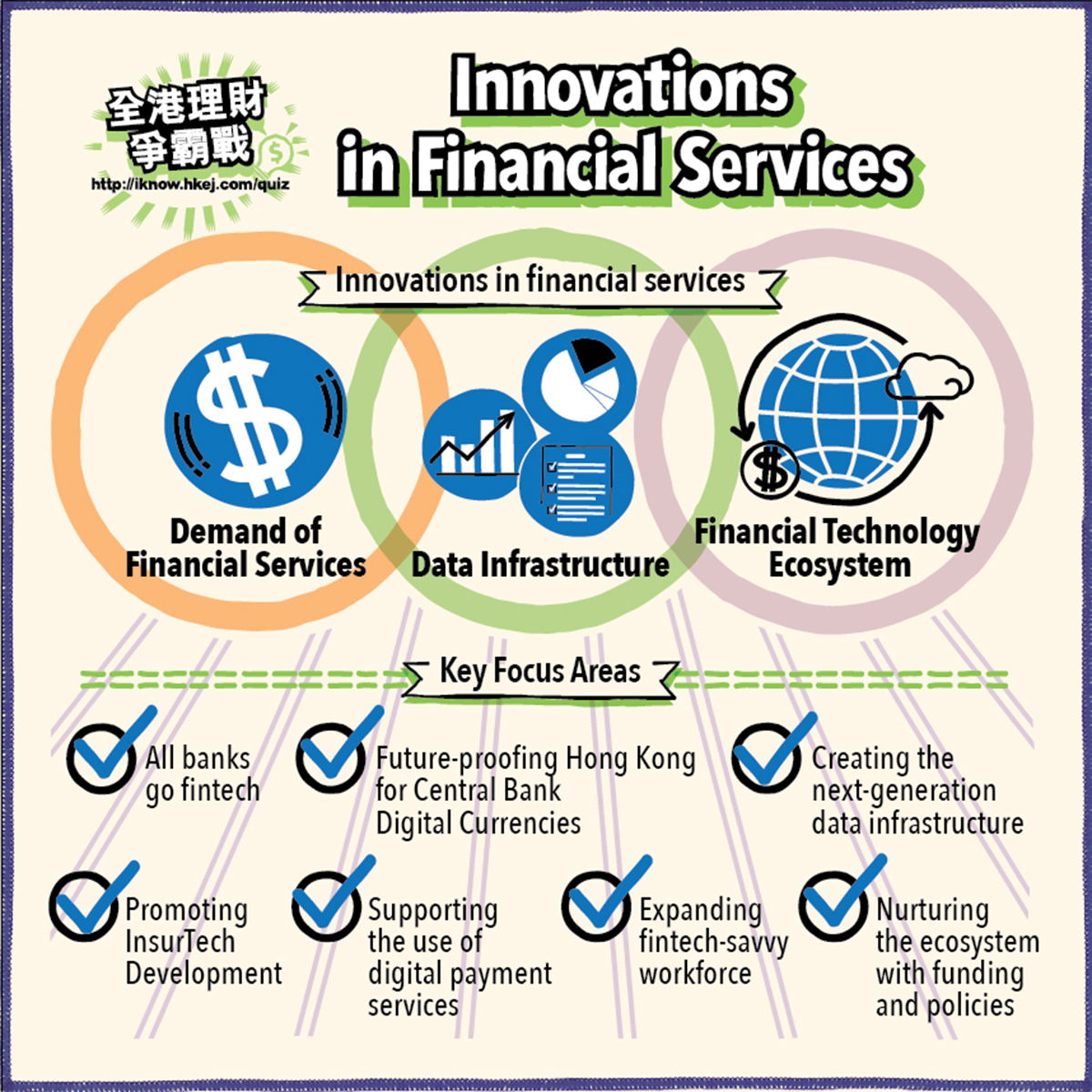

Financial technology (also known as fintech) not only drives innovation in financial services globally, but also changes the nature of commerce and end-user expectations for financial services. While the term fintech may carry different meanings, it is now commonly considered to cover digital banking, data science, digital asset and wealth management, insurance technology (insurtech), and payment services. This article will illustrate how innovations in financial services can facilitate the healthy development of the fintech ecosystem in Hong Kong and promote Hong Kong as a fintech hub in Asia.

With the development of digitalization of banks in Hong Kong, banks provide banking services through various digital channels including internet banking, mobile apps and self-service facilities (such as ATMs and smart self-service kiosks, etc.).

With just a mobile phone, customers can enjoy one-stop banking services conveniently and efficiently, such as fund transfer, cross-border remittance, opening bank accounts, applying for credit cards and loans, investing, purchase of insurance products, etc. Both customers and banks can save time and costs, achieving a win-win situation.

Data science application refers to the consolidation of some valuable data to the enterprise through a series of data programs (such as Python, SQL, C++, Scala, Java, etc.) or artificial intelligence (AI), so as to put forward business analysis and suggestions. This not only reduces manual operations but also automates the business. Data storage and collation can facilitate enterprises to dig out more useful information, which helps to improve the profitability and efficiency of financial services and companies.

Take Commercial Data Interchange (CDI) as an example, financial institutions, with the consent of data owners, can retrieve enterprises’ commercial data, in particular the data of small and medium-sized enterprises (SMEs), from both public and private data providers, to digitalise and streamline a wide range of financial processes, such as Know-Your-Customer (KYC), credit assessment, loan approval, and risk management.

Distributed Ledger Technology (DLT) generally adopted in crypto-assets offers attractive features such as being tamper-proof, immutable and transparent. So far, interest in DLT application has largely been associated with crypto-assets like bitcoin and non-fungible tokens (NFT), but there is more than that. DLT can also be deployed to existing products and processes in the financial markets, such as bond issuance and trading. The tokenised green bonds issued by the Government is a case in point. DLT, if under proper regulation, is expected to enhance efficiency and transparency in finance and commerce, facilitate interaction among parties, substantially reduce cost, and make possible end-to-end automation, which in turn will reduce or resolve existing frictions across clearing, settlement and payments.

As regards wealth management, more financial institutions are adopting artificial intelligence. For example, "robo-advisor" analyses relevant data, such as customer's investment objective, risk preference and financial information, and make recommendation on investment strategies.

Insurtech refers to the use of innovative technologies such as AI and big data analysis to design more personalized and competitively priced insurance products; improve efficiency of product development, risk pricing, distribution, and claims settlement; as well as reducing costs and underwriting risks.

With the advancement of technology and the popularization of smartphones and mobile apps, many insurance apps have emerged, offering services including product inquiries, product purchase, making claims and after-sales services. Some apps are even equipped with AI chatbots or online customer service agents to answer customers’ questions around the clock.

Digital payment service applications simply refer to payments and fund transfers conducted digitally by using e-wallets and mobile apps.

Near-field communication technology (NFC) and magnetic secure transmission technology (MST) are well-developed. In the future, the further applications of technology in payments will better support payments in a cross-border or real-time manner, e.g. for e-commerce.

Little Thrifty enjoys running and cycling, and he’d like to purchase insurance products and services to protect himself. With the popularization of AI and big data, Little Thrifty can now choose “micro” insurances such as “Running Insurance” and “Bicycle Insurance” that meet the diverse needs of individuals more precisely and purchase the insurance products directly through a mobile app. With the application of insurtech, users can quickly and easily understand the scope of coverage of an insurance product and purchase insurance products conveniently, while insurance companies can evaluate the risks of underwriting using big data to comprehensively improve the efficiency of insurance application and underwriting.

Financial Knowledge

Life Events

Contact Us

In support of the Hong Kong Money Month

Copyright © 2023 Hong Kong Economic Journal Company Limited. All rights reserved.