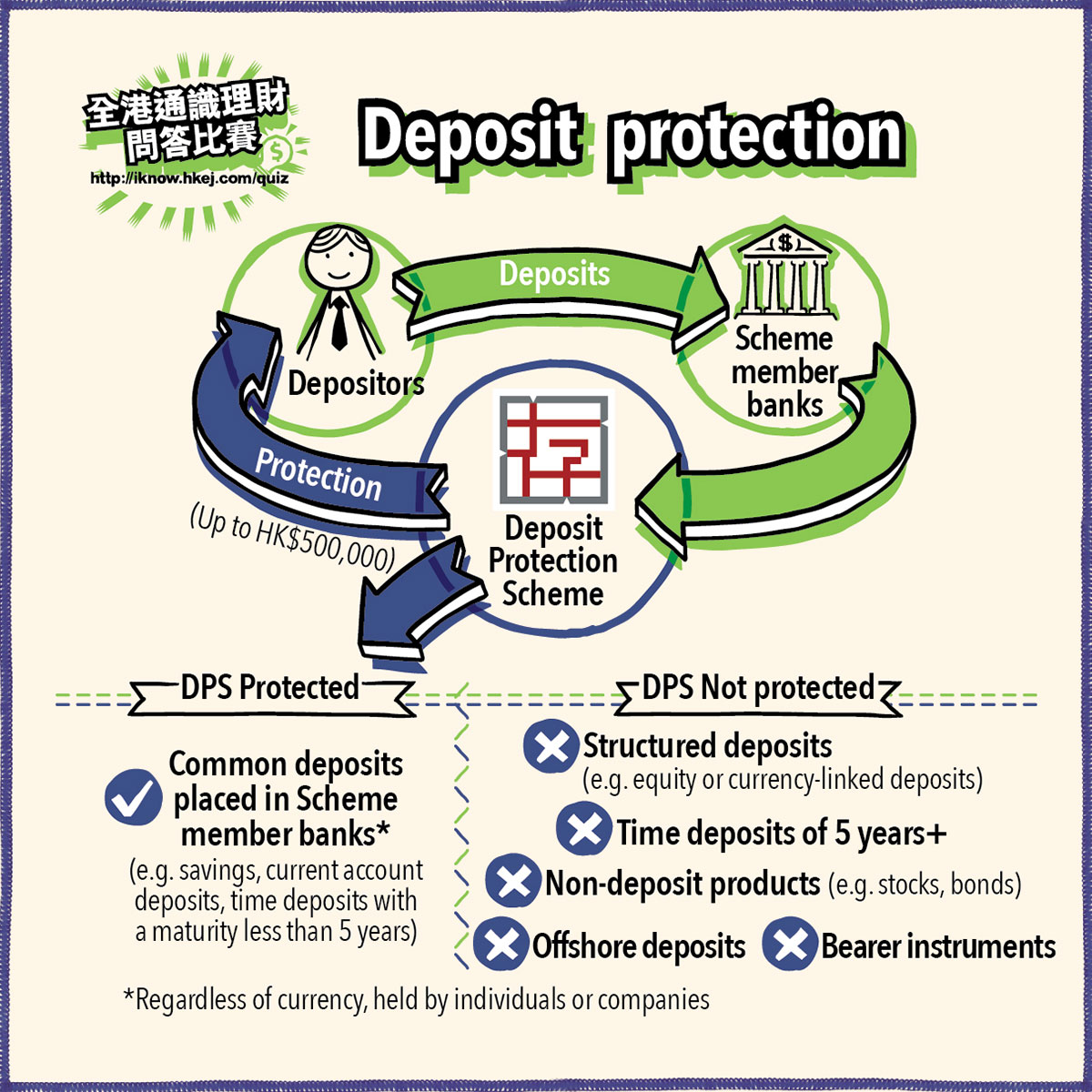

Deposit protection means that when a bank closes down, depositors will be compensated a certain amount, the purpose of which is to maintain the stability of the banking system. Established under the “Deposit Protection Scheme Ordinance” (DPS Ordinance), the Deposit Protection Scheme (DPS) in Hong Kong offers deposit protection up to a maximum of HK$500,000 to each personal and corporate depositor of a member bank. Deposits denominated in Hong Kong dollars, Renminbi or any other currencies are protected.

However, certain deposit categories including time deposits with a maturity longer than 5 years, offshore deposits, structured deposits (such as foreign currency-linked and equity-linked deposits), bearer instruments, and non-deposit products (such as stocks, bonds, warrants, unit trusts, mutual funds, insurance products, and stored value facilities) are not covered by the Scheme.

The public may have the following questions about the Deposit Protection Scheme:

The DPS is funded by contributions paid by Scheme members, not government funds. Depositors are not required to pay for the protection. The DPS is operated by the Hong Kong Deposit Protection Board. The Board is an independent statutory body established under the DPS Ordinance.

The current protection amount of HK$500,000 was set after a public consultation in 2009. It’s believed that the DPS is able to provide full protection to about 90% of depositors, which is in line with international standards. The Scheme aims to pay the depositors full compensation within seven days in most cases. To this end, Hong Kong Deposit Protection Board has always maintained adequate resources through maintaining a highly liquid portfolio of assets and a robust standby credit facility from the Exchange Fund.

Little Thrifty is having a chat with his dad about the household financial situation. Dad mentioned that emergency reserves are very important for unexpected events, such as unexpected medical bills, emergency home repairs, etc. Dad has accumulated HK$500,000 of bank deposits for emergency needs.

“Would you lose your savings if the bank closed down?” Little Thrifty asked.

“My savings of HK$500,000 including time deposits of 3-year tenor and foreign currency deposits are protected by the Deposit Protection Scheme. However, the Scheme doesn’t cover the stocks and bonds I hold.” Dad replied. Though Little Thrifty only has HK$5,000 in his bank account, his deposits are also protected under the Deposit Protection Scheme.

Financial Knowledge

Life Events

Contact Us

In support of the Hong Kong Money Month

Copyright © 2023 Hong Kong Economic Journal Company Limited. All rights reserved.