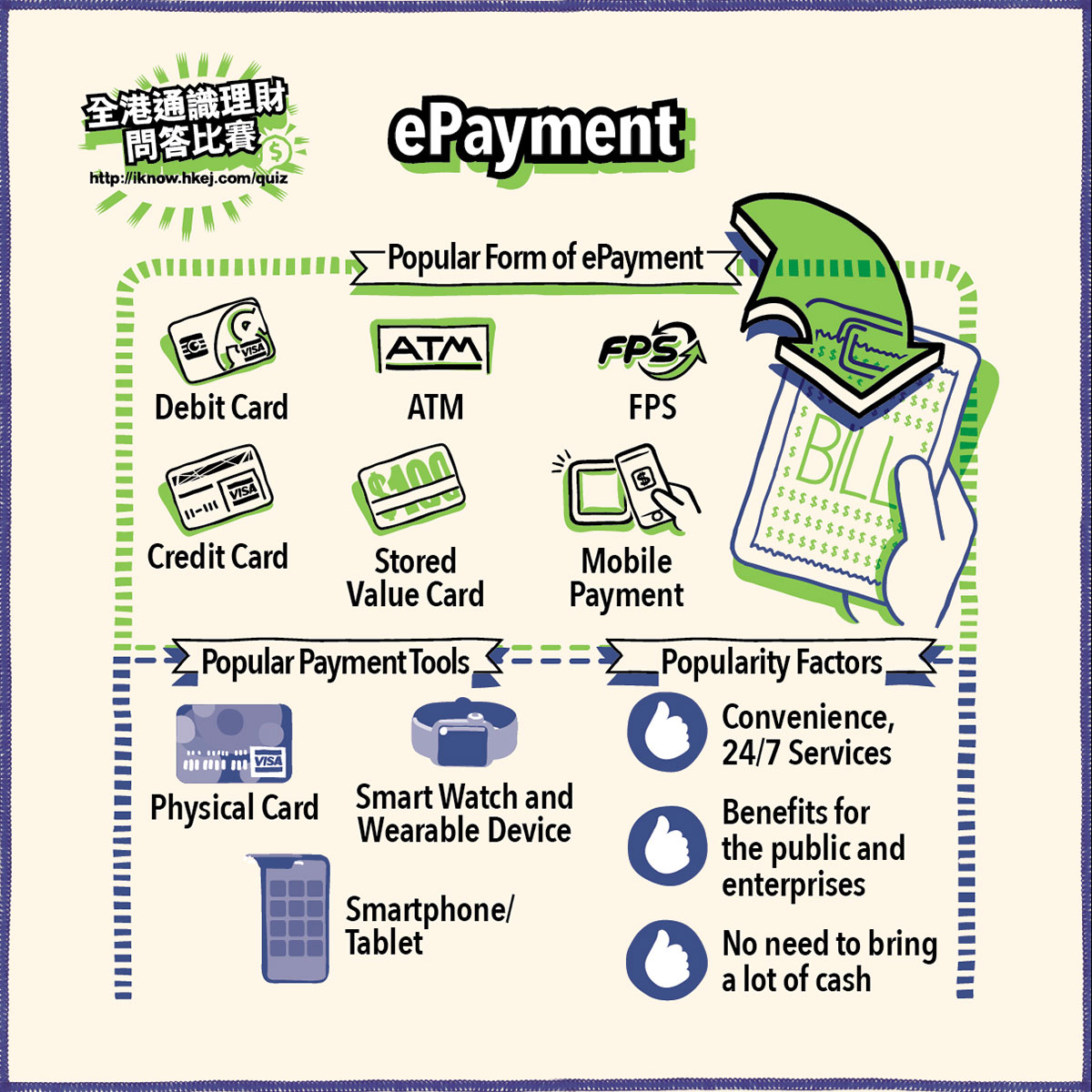

With the advancement in technology and customers’ rising expectations in using financial services, cash is no longer the most dominant form of payment. The usage of non-cash ePayment such as credit cards, debit cards, and mobile payments makes life easier and safer.

Different ePayment methods have different features and usage considerations. Students should make choices based on security, popularity, and personal financial needs in different situations. At present, the more popular ePayment methods are as follows:

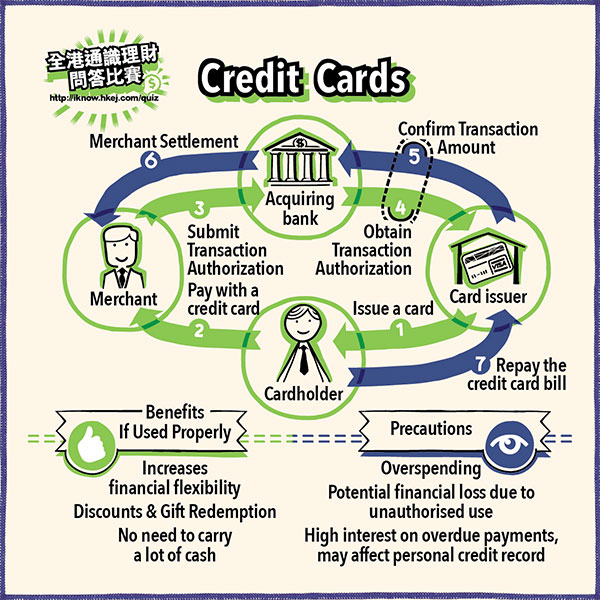

Cardholders can purchase goods or services within the approved credit limit and pay the bills at a specified time (repayment). There is an "interest-free" repayment period if cardholders repay on or before the payment due dates, otherwise, interest and charges will be incurred. Cardholders can also make cash advance transactions with credit cards, but banks usually charge a higher interest rate on cash advances than on the outstanding balance of retail purchases.

Unlike the "Buy now pay later" feature of credit cards, cardholders must ensure that the account linked to the debit card (such as a deposit account) has sufficient funds to complete the transaction, as the money is immediately deducted from the linked account when performing the transaction. EPS is an example.

SVC functions like a debit card in which transactions can only be made when there is deposit, but there is a minor difference that SVC does not link with a deposit account. It deducts money directly from the monetary value stored on the card itself. Octopus Card is an example.

Users can use ATM cards to access banking services through automated teller machines, including bill payment. Since the money is transferred directly from the user’s bank account; it is necessary to have sufficient funds in the account to complete a transaction.

With the emergence of internet banking and mobile devices like smartphones or tablets, mobile payments are gaining popularity. Examples of mobile payments include NFC which allows mobile phone and proximity card reader to transmit and exchange data packets at very short distances (such as Apple Pay and Android Pay); contactless payment that uses contactless-enabled credit cards or devices; payment made by e-wallet mobile apps with QR code and so on.

HKMA announced the launch of the Faster Payment System (FPS) in September 2018. The FPS connects different banks and stored-value facility (SVF) operators on the same platform and operates on a round-the-clock basis. It enables the public to transfer funds across different banks or SVFs with the use of mobile number or email address, and funds available almost instantly. In addition to Hong Kong Dollar (HKD), the FPS also supports Renminbi (RMB) payments. The FPS aims to provide the public and enterprises with more efficient and convenient payment services, and further strengthen Hong Kong's status as an international financial centre.

Little Thrifty is going to join a study tour in London during the summer holiday. Based on the experience of the tour to Shanghai last year, he believes that as long as he has sufficient funds to facilitate financial transactions from his mobile wallet, he needs not carry too much cash for the sake of security.

However, Little Thrifty’s cousin reminds him to pay attention to the payment methods and tools commonly used in different countries. For instance, mobile payments are very popular in China, consumers use mobile payments even for buying groceries. However, debit cards, credit cards, and cash are more popular forms of payments for daily consumption in Europe and America. Mobile payments are not popular among small merchants or small consumptions. Therefore, Little Thrifty’s cousin suggests him to plan the travel budget, exchange sufficient British pounds, activate the overseas ATM cash withdrawal function in advance and set the overseas ATM daily cash withdrawal limit.

Financial Knowledge

Life Events

Contact Us

In support of the Hong Kong Money Month

Copyright © 2023 Hong Kong Economic Journal Company Limited. All rights reserved.