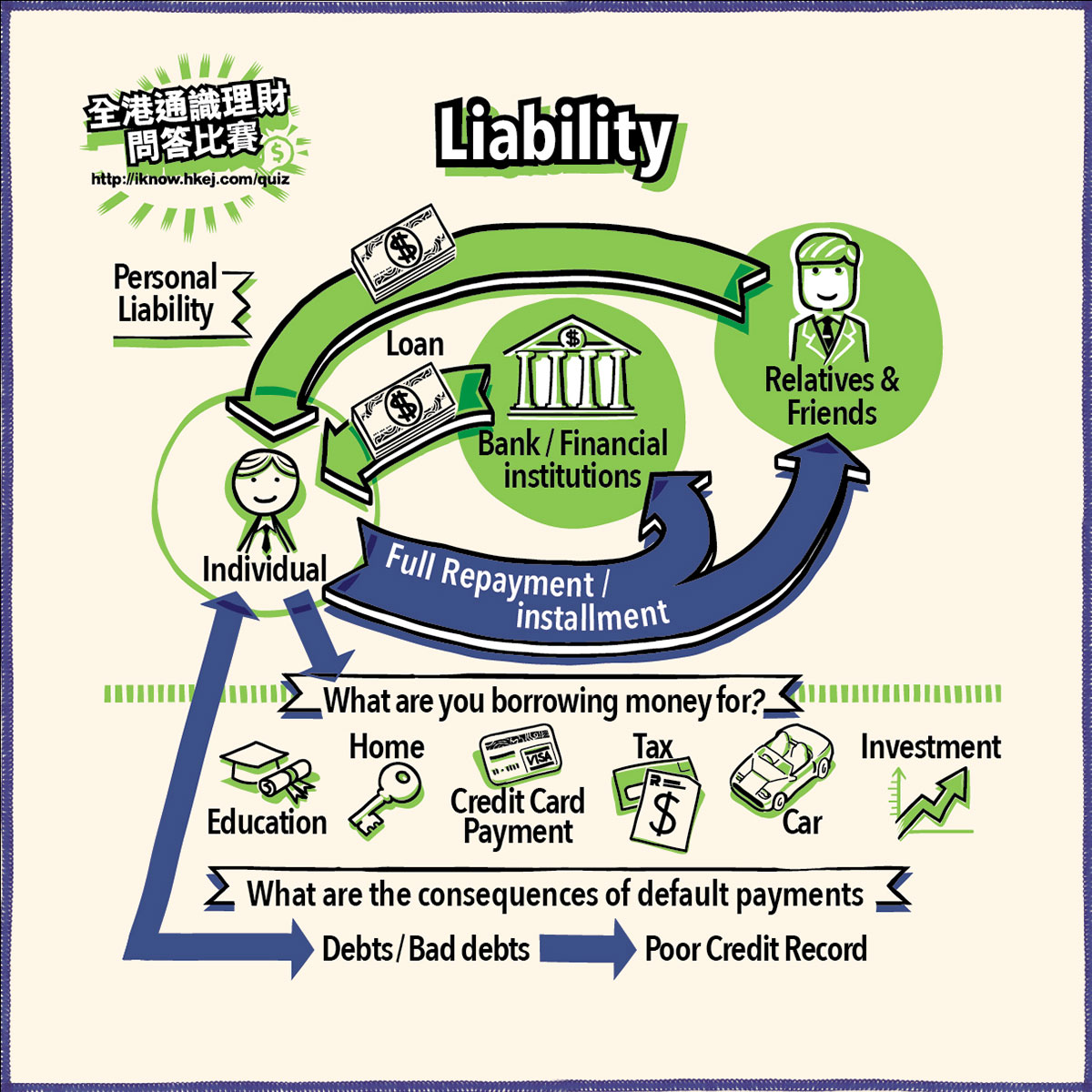

Liability refers to a sum of money an individual or a company owes from banks, another person or other institutions for business or transaction, and such an individual or company is responsible for repaying related debts.

A mortgage is a loan from a bank that helps a borrower purchase a home. The borrower uses the home itself as collateral for the mortgage, and borrows the balance other than the down payment, then repays the arrears in monthly installments until the full amount is paid off. A mortgage is a long-term secured loan spanning as long as 25 to 30 years. If a borrower fails to repay the mortgage, the bank is entitled to seize and sell the mortgaged property. It is necessary to evaluate your repayment ability before taking out a loan.

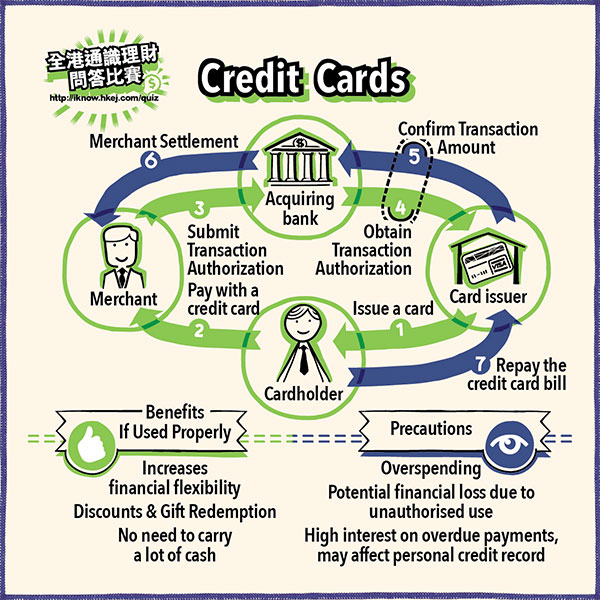

Credit cards enable consumers to “buy now, pay later”. When cardholders use credit cards for shopping, business or travel, the money is paid by the bank in advance and cardholders enjoy an interest-free repayment period. Finance charge will be levied if a cardholder fails to repay the outstanding balance in full and pay only the minimum payment amount. New transactions will also immediately incur finance charge and the snowball effect of interest accumulation may result in crushing debts.

Besides, there is no “interest-free” repayment period for cash advances, which means interest will be incurred from the date the cash advance is made.

Personal debt refers to tax loans, car loans, or any personal loans for unexpected expenses. One should note that all loans come at a cost of interest. If the debt is not managed well, it can become a heavy financial burden.

Corporate liability refers to the capital borrowed from a bank for business growth, accounts payable, or money owed to suppliers and service providers (e.g. audit services) by a company. Corporate’s repayment capability could be affected by the deterioration of the economic environment, rising interest rates, and even customers in arrears.

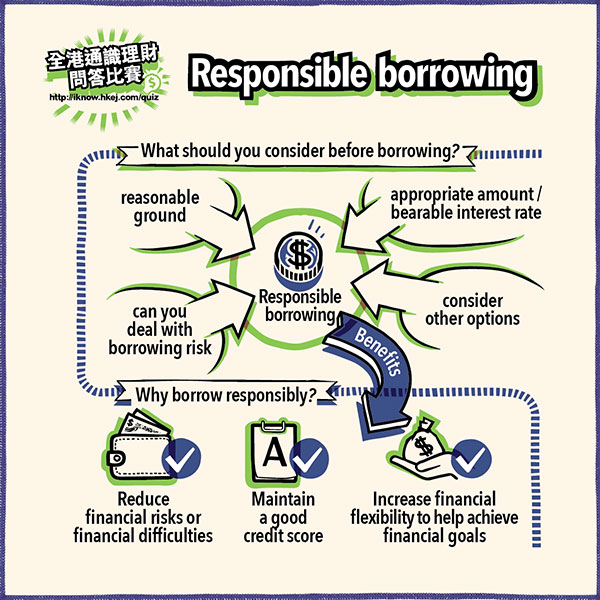

Regardless of individuals or enterprises, responsible borrowing can help us in financial management and business development. However, excessive borrowing or poor debt management could create a heavy financial burden and impact. If there were overdue or missed repayments, and thus poor credit records, it may become difficult to borrow money in the future. You may be subject to a higher interest rate, or get a smaller loan approved, or even your loan application may be rejected.

Little Thrifty bought the latest smartphone and tablet worth HK$20,000, and paid with his credit card. The monthly interest rate of his card is 2.5% (Annualised Percentage Rate (APR) of 35%), and there is no further transaction, annual fee and other fees in his credit card account. If he chooses Plan A, and pays the "Min-Pay" in each statement period (usually refers to the sum of all interest, fees, and at least 1% of the outstanding principal, or a specified minimum repayment amount), it will take him 26 years to pay off the bill.

Even if he chooses Plan B and pays HK$849 in each month, it will take him 3 years to fully pay off.

| Repayment amount per month | The time required to clear the outstanding balance | Total expenditure (principal + interest) | Interest |

|---|---|---|---|

| A. Min-Pay Amount | 26years | HK$67,536 | HK$47,536 |

| B. HK$849 | 3years | HK$30,565 | HK$10,565 |

Financial Knowledge

Life Events

Contact Us

In support of the Hong Kong Money Month

Copyright © 2023 Hong Kong Economic Journal Company Limited. All rights reserved.